CASE starts to publish a quarterly update on Credit Impulse

The notion of Credit Impulse has been introduced for the first time by Michael Biggs, in “The Impact of Credit on Growth,” Global Macro Issues 19 Nov 2008. It represents the change in the change in credit expressed as percentage of GDP and it is considered as a key driver of economic growth. It is calculated in the following steps:

- Take the variation of the stock of loans held by the non-financial private sector (Nonfinancial Corporations and Households & NPISH) on a quarterly basis. We use a quarterly frequency to avoid too many adjustments

- Normalize by nominal GDP on a quarterly basis

- Apply YoY change to that normalized quantity then multiply by 100

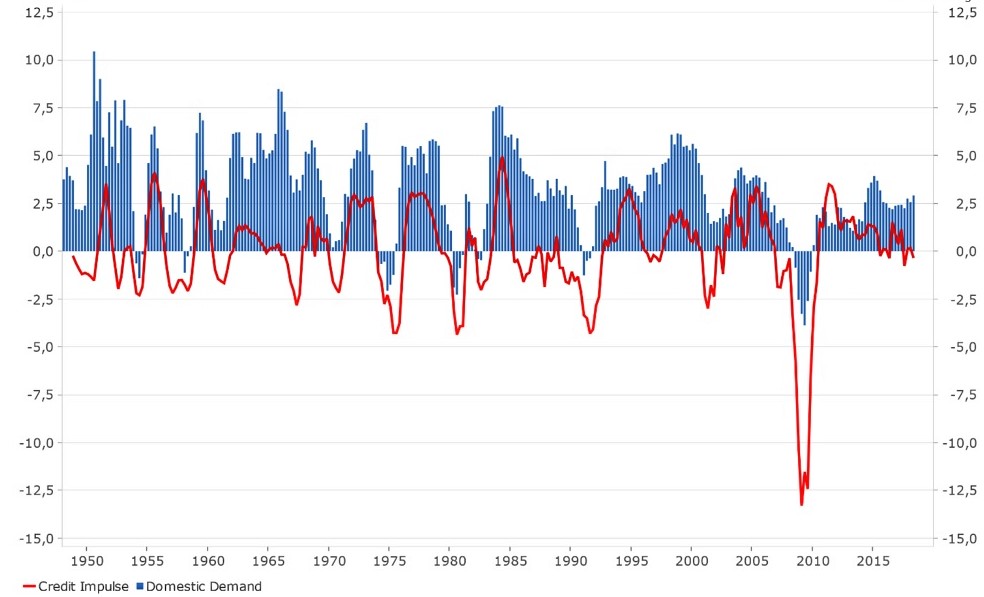

The starting point for the idea of Credit Impulse is the observation that economic recovery can happen without a rebound in credit while a decline in credit is related to a slowdown in economic activity (Calvo et al., 2006). This paradox appears when the stock of credit is compared to the flow of economic activity. Instead of focusing on the stock of credit, Biggs (2008) indicates it is more important to focus on the flow of credit to understand the business cycle. He argues that since spending is a flow, that is financed through new loans, it should be compared with net new lending – also a flow – rather than credit outstanding – a stock. As the flow of loans is increasing, spending is likely to continue to grow and to fuel economic activity. On the contrary, decelerating credit impulse will produce slower economic activity and negative credit impulse will tend to lead to sharpest slowdowns.

In addition, it has been demonstrated that, for many time periods and countries, a strong correlation exists between Credit Impulse and other economic data, especially private sector demand (Biggs et al., 2010). It is also a useful predictive indicator of GDP growth and other macroeconomic data that works with a lag of nine to twelve month (Ermisoglu et al., 2013).

Before the Global Financial Crisis, the United States, Japan and Europe were the main drivers of global credit cycle but, since 2009, a major shift has happened resulting in China becoming the dominant actor. According to the World Bank calculations, China’s contribution to global growth is reaching 35% for the period 2017-2019, matching that of the United States, India and Eurozone together. It is also the world’s largest consumer of industrial metals, accounting for about half of global demand. As a result, China credit impulse is key to monitor to assess the evolution of the global economy. Each time it has turned positive, it has precipitated positive economic changes in China, Emerging market countries and at the global level, and vice versa.

To identify turning points in the business cycle, CASE publishes a quarterly update on Credit Impulse focusing on the main global economies (the United States, China and the Euro Area). From 2019, it will also include an update on the evolution of the flow of credit in Central and Eastern Europe. Credit Impulse analysis and data is contributed by Christopher Dembik, CASE Fellow and Head of Macroeconomic Research at the Danish investment bank Saxo Bank in Paris, France.

References

Biggs, M., (2008), “The impact of credit on growth”, Global Macro Issues 19, November

Biggs, M., Mayer, T. and A. Pick (2009), “Credit and economic recovery”, De Nederlandsche Bank,

Working Paper No. 218/2009

Biggs, M. and Mayer, T. (2013), “Bring credit back into the monetary policy framework!”, Political Economy of Financial Markets, August

Calvo, G. A., Izquierdo, A., and Talvi, E. (2006), “Phoenix miracles in emerging markets: Recovering without credit from systemic financial crises”, NBER Working Paper 12101

Ermisoglu, E., Akcelik, Y. and Oduncu, A. (2013), “Nowcasting GDP growth with credit data: Evidence from an emerging market economy”, Borsa Istanbul Review 13

Read more on this topic:

China is easing again as global growth is slowing

Where is the global economy heading in 2019?

The case for a rebound in global growth in Q1-Q2 2020 is getting stronger